.svg)

Spending hours every week chasing transaction mismatches and failed validations across pipelines, businesses face growing concerns around data integrity, reporting accuracy, and compliance risk. While a governance platform is the answer, choosing the right one is complex in fintech.

This is where knowing how to rank data governance platforms for fintech risk and compliance becomes critical. Instead of feature lists or vendor reputation, reviewing scored options ensures alignment with regulatory needs, traceability, and real-time risk control.

This guide covers key frameworks and criteria to rank platforms based on risk coverage, compliance readiness, and real-world performance.

What Does "Ranking" Mean for Data Governance Platforms in Fintech?

Every fintech operates within a unique mix of risk exposure, regulatory obligations, and operational constraints. Ranking, in this context, is a structured evaluation of how well a platform addresses these realities and integrates with existing data systems, workflows, and compliance processes.

In short, the focus is on clearly defined, risk-critical criteria, rather than measures of popularity or brand size.

Risk Coverage vs Feature Checklists

| Aspect | Risk Coverage | Feature Checklist |

|---|---|---|

| Evaluation Focus | Focuses on how well the platform identifies and mitigates real risks. | Focuses on the number of features available, regardless of impact. |

| Prioritization | Prioritizes capabilities based on risk severity and regulatory impact. | Treats all features as equally important in evaluation. |

| Real-World Relevance | Maps directly to actual risk scenarios and compliance needs. | Often includes features that may not be used in practice. |

| Decision Making | Helps teams choose tools that reduce exposure and improve control. | Can lead to decisions based on volume rather than value. |

| Outcome | Improves risk readiness and strengthens compliance posture. | Creates a false sense of coverage without addressing key risks. |

When platforms advertise extensive features, it doesn't necessarily mean they offer effective risk reduction. Risk coverage addresses vulnerabilities, whereas feature checklists are capability lists without operational context.

Platforms should not just check boxes; they must rank well in terms of how they prevent actual risks.

Scenario! Platforms might claim "data lineage" capabilities, but can they trace cryptocurrency transactions across wallets for AML compliance?

Risk coverage evaluation focuses on selecting tools that protect against real threats.

Compliance Readiness vs General Governance

| Aspect | Compliance Readiness | General Governance |

|---|---|---|

| Configuration Time | Setup takes 2–4 weeks using pre-built templates and workflows. | Setup takes 3–6 months due to custom configuration needs. |

| Regulatory Updates | Regulatory frameworks update automatically within the platform. | Teams must track changes and update policies manually. |

| Audit Support | Pre-built evidence packages and audit trails are readily available. | Teams must create reports and compile audit evidence manually. |

| Staff Requirements | Business and compliance teams can manage the platform with ease. | Technical specialists are needed to configure and maintain workflows. |

| Validation Speed | Testing can begin immediately with pre-configured controls. | Testing starts only after extended setup and configuration. |

Many governance platforms offer basic controls like role-based data access, policy definitions, and data classification. But when tailored to fintech use cases, general tools can slow implementation and fall short of regulatory needs. Businesses instead need automated reporting, evidence collection, and audit trails built for fintech regulations.

To rank data governance platforms for fintech risk and compliance, teams need a framework that evaluates criteria tied to compliance readiness.

Context! To flag suspicious transactions, a business may adopt automated GDPR request handling and PSD2 API monitoring. Using general governance platforms for this can take months of customization, with little room for error.

Why One-Size-Fits-All Rankings Don't Work

No two fintechs operate under the same mix of risks, regulations, and operational demands. A universal ranking overlooks how these differences shape governance priorities and evaluation criteria.

As a result, the same platform can perform very differently depending on context.

- Regulatory variance creates different priorities: Compliance requirements vary across regions and categories, which shifts which governance capabilities matter most. What is critical in one regulatory environment may be optional or irrelevant in another.

- Business model impacts governance needs: Different operating models require different controls, data flows, and monitoring mechanisms. This makes fixed, one-size rankings inherently misleading across use cases.

Rank Data Governance Platforms for Fintech Risk and Compliance

A clear ranking needs a structured framework that considers a range of risk-critical dimensions. Platforms need to be scored based on all key criteria's impact levels, the reasoning, and where it's seen.

| Dimension | Impact Level | What’s Being Evaluated | Examples in Effective Governance |

|---|---|---|---|

| Regulatory Compliance & Audit Readiness | High | Ability to meet regulatory requirements and produce audit-ready outputs. | Automated audit trails and evidence logs Pre-configured compliance reporting |

| Data Lineage & Traceability | High | Visibility into how data moves across systems and transformations. | End-to-end transaction traceability Root cause analysis across pipelines |

| Policy Enforcement & Access Controls | High | Strength and consistency of governance policy enforcement. | Role-based and attribute-based access controls Automated violation alerts |

| Risk Monitoring & Issue Escalation | High | Ability to detect and respond to risks proactively. | Real-time anomaly detection Automated escalation workflows |

| Real-Time & High-Volume Data Support | Medium | Capability to handle streaming and large-scale data environments. | Monitoring high-throughput pipelines Low-latency validation checks |

| Explainability & Evidence Generation | High | Ability to explain decisions and generate compliance evidence. | Audit-ready reports Clear lineage for regulatory reviews |

| Operational Integration | Medium | How well the platform fits into existing tools and workflows. | Integration with ETL, BI, and compliance systems Workflow automation across teams |

| User Experience & Adoption | Medium | Ease of use for business, compliance, and engineering teams. | Intuitive dashboards and workflows Faster onboarding and adoption |

Practitioners consistently highlight that governance only works when it translates into operational visibility and action. As Reddit user data_dude90 noted, "Without trust in data, decision making becomes risky, and outcomes can be costly."

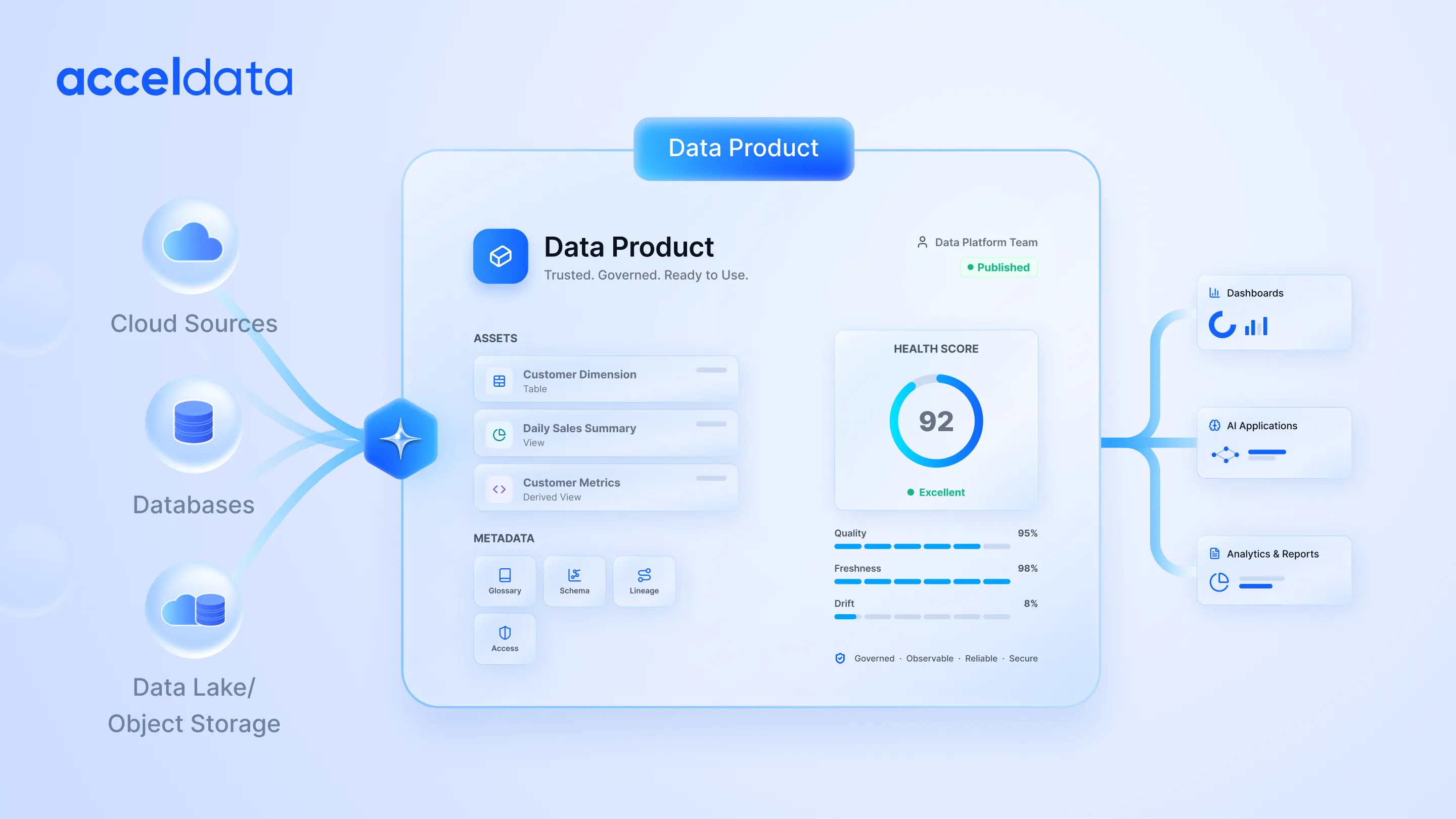

This is where platforms that unify observability, lineage, and quality begin to stand out. Acceldata's data observability for financial services is a popular pick in facilitating proactive risk management and driving compliance with transparent agentic workflows.

Key Criteria to Rank Data Governance Platforms for Fintech

A clear set of must-haves from data governance platforms guides the ranking process. It also helps define the level of investment and pricing model that makes sense for the business. Here are a few criteria that should be non-negotiable.

Regulatory Compliance and Audit Readiness

Adapting to policy updates, both regulatory and internal, is fintech governance 101. With policies changing across regions and frameworks, even small gaps can lead to penalties, failed audits, or reporting delays. This makes compliance readiness a high-impact criterion directly tied to business continuity.

Effective data governance systems operationalize compliance through consistent enforcement and traceability. High-performing solutions enable rapid policy updates, propagate changes across systems automatically, and maintain alignment without disrupting operations.

- Automated policy enforcement that applies regulatory rules across pipelines and flags violations in real time

- Pre-configured fintech control libraries that reduce setup time and align with common regulatory frameworks

Data Lineage and Transaction Traceability

| Stage | Nature of Usual Transactions | How It Becomes/Stays Traceable |

|---|---|---|

| Ingestion | Payment initiation, API calls | Unique transaction IDs, source system tags |

| Processing | Validation, enrichment, routing | Transformation logs, decision trees |

| Storage | Database writes, cache updates | Version control, change data capture |

| Analysis | Aggregation, risk scoring | Calculation lineage, model versioning |

| Reporting | Regulatory submissions, dashboards | Output mapping, recipient tracking |

A single transaction passes through multiple systems, transformations, and checkpoints before it appears in reports. Without clear visibility, validating accuracy or investigating discrepancies becomes difficult. This makes lineage critical for maintaining both operational integrity and compliance confidence.

Strong governance capabilities provide end-to-end traceability across this lifecycle. Mature systems go beyond static lineage by offering real-time observability into transformations, dependencies, and the downstream impact of changes.

Risk Monitoring and Issue Escalation

Financial anomalies, delays, or inconsistencies, when left undetected, can affect transactions, reporting accuracy, and compliance outcomes. This makes proactive risk monitoring a critical capability for operational stability.

Effective systems identify issues in real time and escalate them with context. High-performing solutions go beyond alerts by surfacing root causes, prioritizing risks based on impact, and enabling faster resolution before problems reach customers or regulators.

- Real-time anomaly detection that identifies deviations across pipelines, volumes, and data quality signals

- Automated escalation workflows that route issues with context, ownership, and severity-based prioritization

Impact: High-performing systems also support composite risk indicators that combine multiple signals. Unusual data volumes, failed quality checks, and access anomalies can reveal deeper issues before they escalate.

Policy Enforcement and Access Controls

Strict access controls and well-defined governance policies are what secure fintech data and transactions. As systems scale, maintaining consistent enforcement across teams and data environments becomes more complex. Gaps in enforcement can lead to misuse, compliance violations, or security risks.

Strong governance frameworks ensure policies are applied uniformly and adapt to changing roles and contexts. Continuous monitoring of access patterns helps detect anomalies and maintain control without relying on manual oversight.

Support for Real-Time and High-Volume Data

Systems operate on continuous streams of high-volume transactions. Governance needs to keep pace without introducing latency or bottlenecks. Delays in validation or data monitoring can directly impact decision accuracy and compliance outcomes.

Scalable systems handle real-time processing while maintaining performance under load. Data validation happens in motion, with low-latency monitoring that supports governance without slowing down core operations.

Explainability and Evidence Generation

Production environments need to be transparent, especially during audits and regulatory reviews. Every data point, transformation, and output should be clearly explainable. Lack of clarity can delay audits and reduce confidence in reported data.

Effective governance provides structured explanations and generates audit-ready evidence. Mature systems make it easy to trace outputs back to source data and present findings in a clear, regulator-friendly format.

Fintech Risk Scenarios Governance Platforms Must Handle

Once the rankings are clear, it's important to consider more detailed everyday situations where data governance solutions will be put to use. Here are a few fintech scenarios where governance capabilities are tested in real time.

Multi-System Transaction Flows

Transactions move through multiple systems, such as data APIs, processors, ledgers, and reporting layers, before final settlement. Each step involves transformations that must remain consistent and traceable to avoid reconciliation issues or reporting errors.

End-to-end lineage tracking ensures visibility across every stage. Real-time validation helps catch inconsistencies early, while traceability makes it easier to identify and resolve discrepancies.

Cross-Team Data Access and Updates

Customer data is accessed and modified by multiple teams across operations, risk, and support. This creates challenges in maintaining consistent access controls, tracking changes, and ensuring compliant usage.

Dynamic access controls regulate who can view or modify data, while continuous monitoring tracks usage patterns. Detailed logs and anomaly detection help maintain compliance and accountability.

Multi-Jurisdiction Regulatory Reporting

Data from multiple systems is aggregated and transformed to meet regulatory reporting requirements across regions. Each jurisdiction may require different formats, validations, and timelines, increasing complexity.

Standardized validation processes ensure data consistency across reports. Clear audit trails and structured workflows support regulatory requirements and enable audit-ready reporting.

How Fintech Teams Should Customize Ranking Criteria

A ranking framework must reflect unique business characteristics, risk appetite, and growth trajectory. Standard criteria often miss nuances like customer types, transaction patterns, and expansion plans, making generic evaluations unreliable.

Regulatory exposure, data architecture, and transaction behavior should directly shape how criteria are weighted. Different markets, system maturity levels, and transaction volumes require distinct capabilities, making context-aware evaluation essential.

Key areas to prioritize while customizing ranking criteria include:

- Regulatory and market context: Weight compliance features based on jurisdictions, customer segments, and reporting obligations

- Operational scale and architecture: Account for transaction volume, latency needs, and system maturity when evaluating platforms

Using Rankings to Shortlist and Evaluate Platforms

Practical evaluation requires translating scores into actionable selection processes. Using platform rankings efficiently in decision-making avoids analysis paralysis.

Creating a Shortlist From Rankings

| Platform Type | Example Vendors | Typical Strengths | Common Limitations |

|---|---|---|---|

| Governance Specialists | Collibra, Alation | Deep governance features | Limited GRC integration |

| Integrated GRC | ServiceNow, MetricStream | Unified risk view | Generic fintech support |

| Modern Data Platforms | Informatica, Acceldata | Technical sophistication | Newer governance capabilities |

Start by establishing minimum acceptable scores for high-impact criteria, like regulatory automation and lineage capabilities. Filter out platforms that fail these thresholds, regardless of their overall scores. Then calculate weighted totals using customized importance factors to identify the top five platforms for detailed evaluation.

The shortlist should include a mix of platform approaches. This typically includes governance specialists, integrated GRC suites, and modern data platforms with governance modules. Comparing these categories helps surface tradeoffs and gives a clearer view of what is a better fit before moving into proofs of concept.

Validating Rankings Through POCs

Proof-of-concept (POC) exercises should replicate real business scenarios using actual data and workflows. Common use cases include customer onboarding, transaction monitoring, and regulatory reporting. This ensures evaluation reflects how the platform performs in day-to-day operations.

Effective POCs go beyond feature checks to assess setup effort, performance under load, and usability across teams. Testing with realistic data volumes, integrations, and user roles reveals how the platform behaves under pressure and where limitations may surface.

To get meaningful insights from POCs, focus on the following:

- Test high-risk scenarios: Simulate audit conditions, data inconsistencies, and system delays to evaluate how the platform detects, handles, and recovers from critical issues under stress.

- Involve business and compliance users: Gather feedback from non-technical teams to identify usability gaps, workflow friction, and adoption challenges that technical testing alone may overlook.

Vendor responsiveness during the POC is also a strong indicator of long-term reliability. The level of support during setup and troubleshooting often reflects the quality of the ongoing partnership.

Aligning Stakeholders on Risk Priorities

Successful evaluation requires aligning technical capabilities with business risk priorities. This means translating platform features into outcomes that stakeholders understand and value.

Risk heat maps and impact scoring help visualize how each platform addresses key risks. These simplify decision-making and make trade-offs easier to communicate at an executive level.

Different stakeholders will prioritize different aspects:

- Legal and compliance teams focus on audit readiness and regulatory coverage

- IT teams prioritize integration, scalability, and performance

- Business teams value usability, adoption, and operational efficiency

Structuring evaluations around these perspectives ensures broader alignment and faster decision-making.

Updating Rankings as Regulations Change

Fintech operates in a constantly evolving regulatory environment, making static rankings quickly outdated. Regular reassessment is essential to ensure evaluations remain aligned with current requirements and business priorities. Establish review cycles to track regulatory updates, platform changes, and strategy shifts.

Major regulatory changes or market expansion should trigger immediate re-evaluation. Vendors should demonstrate proactive regulatory tracking and clear update mechanisms. Platforms that incorporate changes automatically reduce manual effort and maintain continuous compliance readiness over time.

Turn Governance Rankings into Real-World Risk Control

Selecting the right data governance platform is best done by evaluating how it provides risk coverage, traceability, and adaptability to address real-world vulnerabilities. Ranking them reflects compliance readiness, customer data security, and a business's ability to mitigate risks like fraud, data quality anomalies, and even regulatory reporting discrepancies.

Platforms that combine observability, automation, and lineage simplify governance and strengthen risk control on every transaction and data flow. Acceldata's Agentic Data Management is a top choice for its agentic workflows that deliver proactive risk detection, continuous compliance, regulatory reporting, fraud detection, and transaction-level visibility.

Thinking of building a governance framework that actually keeps up with fintech complexity? Book a demo call with Acceldata today.

FAQs about Ranking Data Governance Platforms for Fintech

How do you rank data governance platforms for fintech risk and compliance?

Rank data governance platforms for fintech risk and compliance by evaluating regulatory automation, lineage capabilities, and risk monitoring features using weighted scoring. Focus on fintech-specific configurations, like real-time processing and multi-jurisdiction support, rather than generic governance features.

What are the most important criteria for fintech governance platforms?

Regulatory compliance automation, transaction-level data lineage, and real-time policy enforcement rank highest. These capabilities directly help avoid fines, maintain customer trust, and support business growth while managing complex financial data.

Rank data governance platforms for fintech risk and compliance — where should teams start?

Begin with regulatory requirement mapping, identifying which compliance frameworks apply to business operations. Then assess current risk exposure and data architecture maturity before evaluating platforms against these specific needs using structured scoring methods.

How is fintech governance different from other industries?

Fintech governance requires real-time transaction monitoring, multi-jurisdiction regulatory compliance, and enhanced security for financial data. It comes with immediate regulatory penalties for governance failures and must balance innovation speed with risk management.

Should fintechs prioritize compliance or flexibility?

Both matter equally. Modern platforms deliver compliance through flexible, automated frameworks rather than rigid controls. Look for solutions supporting compliance policy-as-code approaches that maintain agility while ensuring regulatory adherence through intelligent automation.

How often should governance platforms be re-evaluated?

Conduct comprehensive platform reassessments annually, with quarterly reviews for regulatory updates and new capabilities. Major business changes like market expansion or new product launches trigger immediate re-evaluation regardless of schedule to ensure continued fit.

Can one platform cover all fintech compliance needs?

While comprehensive platforms address most requirements, specific use cases may need specialized tools. Focus on platforms covering 80% of needs through native capabilities, ensuring strong integration frameworks for specialized additions when necessary.

How should fintech teams validate rankings before purchase?

Run proofs-of-concept using real data and scenarios, involving actual users throughout testing. Validate vendor support quality, implementation timelines, and total cost of ownership beyond licensing fees. Request references from similar fintech companies for practical insights.